Suez Canal and Emerging Markets

The conflict in the Red Sea has disrupted the Suez Canal but does it actually matter, who is impacted, and what about the oil?

In 2021, the Ever Given became lodged in the Suez Canal halting ingress and egress for six days. The costliest “traffic jam” in history set back the world economy by $400 million per day according to some estimates. The Ever Given demonstrates how interconnected and complex supply chains became under the old global order. It was chartered by a Taiwanese company, registered in Panama, owned by a Japanese company which itself was owned by a conglomerate, and employed a German technical manager leading a crew of mostly Indian nationals.

Last week, a Red Sea drone attack caused a small fire on a Maersk vessel halting passages and bringing the normally boring shipping corridor back into focus.

In this edition of the Emerging Real Estate Digest, we’ll take a look at the history and significance of the Suez Canal, followed by a brief discussion on oil, and end by looking at the impact of its disruption on selected emerging market economies.

History & Significance of the Suez Canal

The idea of a waterway-connecting canal in Egypt dates back at least to the days of the Pharaohs. On November 17, 1869, the Suez Canal was christened providing a new 164 km (i.e., 102 miles) long and 56 m (i.e., 184 feet) wide shipping route between the Mediterranean and Red Seas. Ferdinand de Lesseps, a French diplomat and businessman, was the brains behind the venture. Tens of thousands of mostly French investors provided the funding, and the land that the canal runs through was granted by Egypt’s leader in exchange for a 44% personal stake in the project. This stake was later sold to the other investors making it almost completely a French affair.

Great Britain strongly opposed the Suez Canal’s construction as it already controlled the longer shipping route around Africa to India, its crown jewel. In 1882, it seized control of Egypt which led to the 1888 Convention of Constantinople to set out the rules for how the French-owned Suez Canal would operate in Egypt under British rule. In 1922, Egypt gained independence but the Brits managed to hold on to control of the Canal until 1956.

The Suez Crisis of 1956 began when Egypt’s President Nasser nationalized the Suez Canal. The canal shareholders, and Great Britain, responded by lodging an offensive with Israel to reassert their claims, take the Sinai Peninsula, and topple Nasser. Controlling the Sanai meant owning the chokepoint’s entire eastern bank.

Egypt was far outmatched, never had a chance, and folded almost instantly. The problem for the Europeans was that the Americans opposed the offensive. They objected because it gave an opening for the Soviets to enter the region with troops, and would push Egypt into the hands of the communist bloc. Seeing the writing on the wall, the victorious forces pulled back, Egypt was made whole, Europe humiliated, and America became viewed by the world as the “new sheriff in town”.

Twelve years later In 1967, Israel came back for more and successfully seized the Sinai Peninsula for itself in a matter of days. Egypt’s leader, Nasser, blockaded the Suez Canal in response and it became a warzone for nearly ten years. In 1975, the Americans cleaned out the canal of mines and wreckages and it was reopened. In 1979, the Sinai Peninsula was demilitarized and returned to Egypt.

In 2014, Egypt invested $8 billion to make the canal deeper and wider and added a second canal parallel to the original. The deepening and widening were required to permit the new mega vessels carrying 25k+ containers to pass through. The extra lane nearly doubled capacity from 51 ships per day to 97. Expanding the canal took one year, compared to the ten it took to build the original.

The Suez Canal matters because it links East and West. Without the canal, ships carrying goods between Asia, Europe, and the Middle East are forced to go around Africa which adds 8 - 20 days and thousands of extra miles to the journey. Note that Africa is much larger in reality than it appears on maps.

Oil Discussion

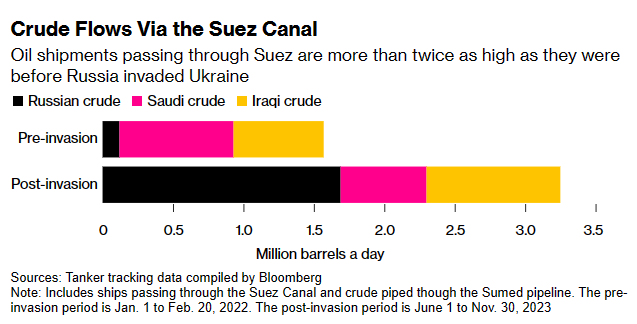

About one-third of the ships that have passed through the Suez Canal in recent years have been oil tankers. On average, they carry 1.5 million barrels per day through the chokepoint, but the numbers have doubled recently as a result of European sanctions on Russian oil. Russian oil, which used to be pumped into Europe via pipelines, is now being shipped through the Suez Canal to be sold to willing buyers in India and China.

Europe receives most of its Middle Eastern oil through the 320 km (i.e., 200 mile) Sumed pipeline connecting the Gulf of Suez with the Mediterranean. The pipeline transports 80% of the oil Europe purchases from the Middle East Gulf and therefore is not significantly energy deprived from a Suez clamping. If it needs more oil, Europe has options.

America still buys oil from the region but not one barrel of the almost 7 billion barrels of oil imported into America since 2022 have gone through the Red Sea or Suez Canal. Half of the imported oil comes from Canada, and ten percent is from Mexico. Saudi Arabia and Iraq contribute about ten percent collectively, followed by Colombia with a three percent share.

China is energy insecure but not due to an overreliance on the Red Sea or Suez Canal. Although 80% of China’s imported oil comes from the Middle East, the shipments originate in the Persian Gulf so avoid the Red Sea altogether. China’s energy issue is that it is running out of oil domestically, and Russia doesn’t have enough to pipe in to make up the difference between what it produces and what it requires. The oil tanked into China goes through a gauntlet, first passing by India, an adversary, and then through the narrow and easily put aflame Malacca Strait which is only 1.5 miles wide at its narrowest point. What’s worse, the oil must then navigate through the contested South China Sea and past rivals Japan and the Philippines.

Besides oil, dry-bulk vessels account for another one-third of shipments and these carry raw materials such as coal, iron ore, and grains mainly to China. The final one-third are container ships carrying mostly finished products from China to customers in Europe. Some of the ships bound for America’s east coast pass through the Suez Canal, but most go across the Pacific to LA’s port to be taken eastward overland, or through the Panama Canal.

Emerging Market Impacts

Latin America. The impact of the Suez Canal closing is nominal to Latin America for two reasons. First, South America is geographically positioned in a way where circumventing Africa doesn’t add more time, distance or cost. By using the Cape of Good Hope fees are avoided and time is perhaps saved by not having to wait to pass through. Brazil is a good example and has become a major exporter to China of soy to feed its pigs, and also corn and oil. Second, shipments from the western side of the Continent would either dip around Argentina into the Atlantic Ocean, or pass through the Panama Canal.

Africa. Closing the Suez Canal would devastate Egypt’s economy. It would lose transit fees which in 2022 amounted to $8 billion and are expected to grow considerably in 2023. China has invested $10 billion+ in building industrial capacity in Egypt because it has the canal and favorable tax agreements with nations in Africa and Europe. These investments would largely fail and future FDI into Egypt less likely. South Africa would benefit from the closure since more ships would pass through Cape Town and would naturally make use of its various maritime services. South Africa would win big geopolitically and become more attractive as a place to invest. East African exports to Europe, for example coffee from Kenya, would be challenged.

Southeast Asia. Finished goods sent to Europe would have higher shipping costs and take longer which could push Europe to look for alternatives. Few intermediary goods pass through the Suez Canal so manufacturing supply chains would be minimally impacted. Raw material inputs from Europe would be negatively impacted, as would agriculture exports from Europe.

My take: The Suez Canal should be seen as a connecter of East and West, Europe to China. The goods that characterize shipments through the canal are (1) finished goods from China to buyers in Europe, (2) raw material inputs and agriculture products to Asia, and (3) oil and gas tanker shipments mainly to Europe, India and China. A closed canal doesn’t starve Europe of energy since 80% of its oil from the region is delivered via pipeline, and disruptions in gas shipments could be balanced with more LNG imports from America. Neither China nor America detrimentally relies on oil shipments from the Suez Canal or the Red Sea.

The winners (if Suez closes indefinitely) are large shippers whose shares are already surging, South Africa’s Cape Town which becomes a relevant sea hub once more, and nations attempting to decouple from China since shipping costs and complexity go up.

The losers are Egypt which is a largely irrelevant country without the Suez Canal, Russian oil and gas shipments to China and India would be more costly, European exporters of agriculture and raw materials to Asia, and Asian importers to Europe of finished goods.