Yesterday, The Meb Faber Show Podcast, published an interview with Sam Zell. My favorite quote from the show:

“For an entrepreneur the word failure doesn’t exist, it just didn’t work out, and you get up off the floor and try again.”

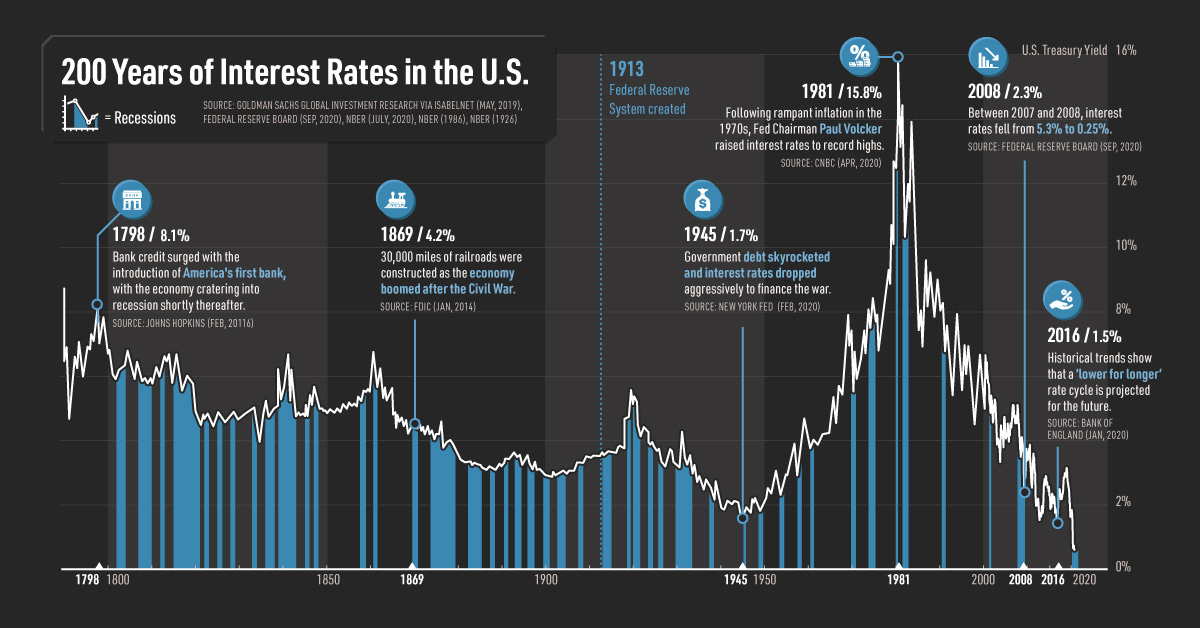

In 1968, Sam Zell founded the Equity Group Investments, a firm which was once the largest apartment and office building owner in America. He sold the behemoth to Blackstone in 2006 for $36 billion. Mr. Zell’s insights are valuable for many reasons, including that he’s invested in real estate during periods of rising interest rates (i.e., 1968 - 1981). How many people in your network can credibly say that?

Pearl 1 | Valuations are still too high

The pricing of real estate assets in America has been for some time beyond what makes sense for Sam Zell. He’s been a seller in that market. Six years ago he took over a $12 billion REIT (i.e., Commonwealth) with most efforts devoted to selling the properties (141 out of 145) into this environment of too much capital chasing too few deals. Private equity funds are run by well-paid professionals incentivized to raise and spend other people’s money.

Spending in Washington DC has made the problem worse. Nothing is more detrimental to the value of real estate than inflation. Mr. Zell’s advice to the bureaucrats:

“…stop spending money you don’t have.”

Pearl 2 | “Liquidity is value”

Real Estate is an illiquid asset, but it is often given the appearance of liquidity by REITs which trade freely in the market, and that the market is flush with investment capital eager to purchase stabilized properties. This illusion only works so long as capital is rushing in. When capital flows slow or stall, these “liquid” investments will put up gates and begin behaving as illiquid assets do.

What is the illiquidity premium of your real estate holdings? Is it enough? Do most REIT investors classify the holding as liquid?

Pearl 3 | Shortage of residential

”Not in my backyard” has becoming a calling card for impairing residential developments. As long as this continues, there will be shortages in housing. The number of people being added to the population exceeds the new residential stock being produced, and that’s because we’ve made it too difficult and expensive to add to the housing supply.

Pearl 4 | Early competition analysis

Every investment analysis for Sam Zell starts with, and ends with, assessing the competition to the business. Who are the competition? How are the competition financed? If things get tough, will the competition lower their prices/rents to the point of eliminating the opportunity?

He wants barriers to entries and moats which include a unique location, patent, structure, and funding source.

Pearl 5 | Don’t be a quant

Numbers say what you want them to say. Deep quantitative analysis is important, but he prefers to know things like what it cost to build the property he’s looking to acquire. This helps him understand what a competitor has to do to build next door and compete with him.

Private equity, and other advisors, rely too much on predetermined and far away (i.e., 5 years or more) exit valuations to make their numbers work and demonstrate return potential to LPs. It’s too difficult for anyone to prognosticate what will happen in the market in five to ten years. He favors one- to three-year predictions.