Part 4: Real Estate Private Capital Series

Emerging Real Estate predicts that private equity will be replaced by private debt and SMAs as the primary mechanisms for international investors to participate in real estate in LATAM and Africa.

In this four-part series we will look at the role of the private capital asset class in real estate investing. Where it’s been, where it’s going, and where the future opportunities lie. Part four will give actionable intelligence you can act on today to get in front of the next wave of private capital into Latin America and Africa real estate investments.

The four parts of the Private Real Estate Capital Series:

✅ The shortcomings of Private Equity for Real Estate Investing

Positioning yourself for the next wave of private capital flows into Latin America and Africa

Private Equity has historically been the primary structure utilized by international institutional investors to tap into emerging market commercial real estate opportunities. Unfortunately, returns have been poor, and we discussed some reasons why this is the case last week. Real estate funds focused on American investments have also underperform producing IRRs of only around 7%.

The status quo of using private equity structures is a problem because it encourages an overcommitment of capital in the regions, resulting in unsustainable waves of investment, with limited ability to pump the brakes once the investment theme comes under pressure.

The example below illustrates the phenomenon of private equity investment waves, into emerging market real estate, and why it’s not preferred.

Colombia Shopping Mall Investor Example

Let’s pretend we’re observing a hypothetical investment wave of capital into private equity funds mandated to develop shopping malls in Colombia. The investors and managers are all based in America.

Phase 1: Early investor enters a ripe opportunity. Likely for years, the investors have been monitoring an opportunity to invest in developing shopping malls in Colombia. They like the low retail saturation rates, high footfall at existing malls, and strong tenant demand for new retail space. The returns are more than suitable and are based on conservative assumptions. The investors decide to pull the trigger. Three years later, the first mall is finished, fully tenanted, and opens to the public. It’s a huge success and excitement builds that the next three projects under construction will also be winners.

Phase 2: More capital mobilizes over a “hot” theme. Noticing the success of the early adopter investor, the finance media hype machine engages and touts the investors as visionaries after having found the next “hot” investment theme, Colombia shopping malls. It’s a topic at cocktail parties, conferences and trade journals. More capital mobilizes and proceeds to flood into Colombia to build more retail space. But this flow of funds encounters a slightly different environment than the preceding. Everything costs a bit more, suitable land more difficult to secure, and tenants are no longer falling over themselves to sign the first lease put in front of them. The tide is starting to go out.

Phase 3: Stalwarts enter based on early fund results. At this stage the first phase fund is closing or has closed, and the returns look attractive. Afterall, it was a smaller investment, into a well-defined investment theme, which had been observed for years and was then ripe. The second phase funds are deploying the last of their capital, and it’s therefore too early to know how those will do so the investors assume they will have returns similar the first.

The third phase funds are the largest yet. The concept is now proven, and no longer a novelty, therefore the pools of capital available broaden and deepen. Private equity managers are heavily incentivized to raise large funds due to higher fees, and the status which comes from raising ever larger funds. They grab as much capital as is possible.

The results are that the third phase funds never had a chance. Rents are lower, prices higher, deals are scarce, and the local competition is also now fully engaged. This largest third phase of the wave is just getting started and ten years of fees for the managers are locked in. The only good news for the investors is they won’t have to worry themselves with having to pay performance fees.

Implications of private equity waves beyond poor returns:

Foreign investors get torched. Not the early ones, they get out just in time. It’s the second, and particularly third phase funds which receive most of the damage.

Sentiment remains low for too long. Having such a bad experience keeps investors away for too long, even after the market has returned to being an attractive investment destination. They invest when and with whom they shouldn’t have, and fail to take action when they should.

Local market left distorted. Fortunes are made locally, and new companies formed to service the private equity cowboys with seemingly unlimited access to capital. The excess supply left in the wake takes years for the market to absorb, negatively impacting local financiers and real estate companies.

Zombie assets. What happens to the zombie assets without interested buyers once the fund life ends?

Private Debt Real Estate Funds

Private Debt Real Estate (“PDRE”) funds may become attractive alternatives for America’s institutional investors to participate in Latin America and Africa real estate moving forward. Credit funds have lower fees, and are less risky than their equity counterparts. Underwriting is stricter and more defendable, whereas equity underwriting is often based on gut feelings, opinions of the local developer and consultant teams, and crystal ball predictions of what the world and company will look like five to ten years in the future.

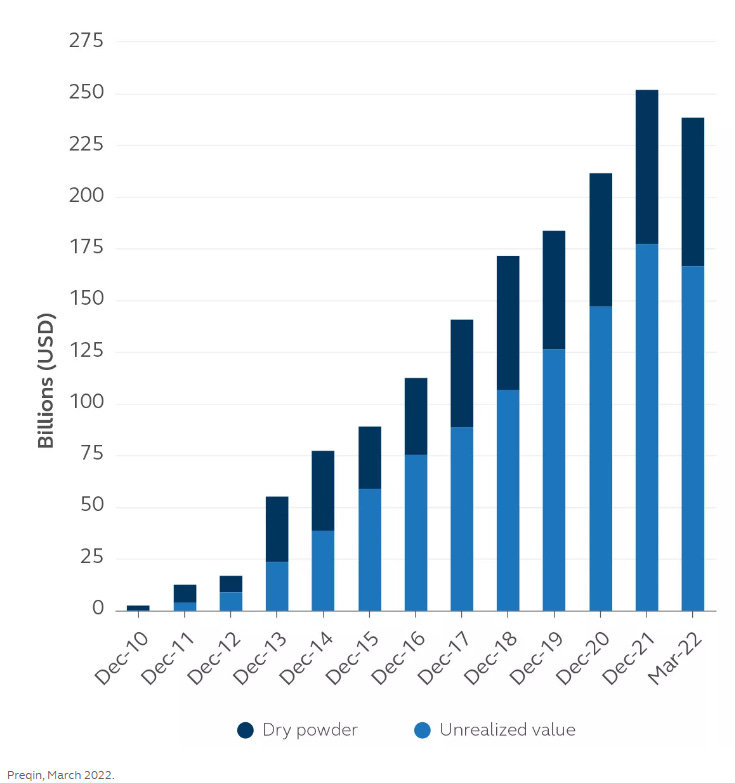

Globally, Private Debt Real Estate funds are exploding, and the new funds being raised are expected to perform exceptionally. These vintages will benefit from higher interest rates, lower real estate entry-point valuations, tighter LTVs, and the potential to gain even more as interest rates come down in the future.

Presently, Private Debt Real Estate funds are virtually non-existent in Latin America and Africa. But the investment theme is gaining steam and the total value of private debt deals announced in emerging markets grew by 89% between 2021 and 2022. The explosive growth has been attributed to banks retreating from emerging market lending during the global lockdowns and deciding to not return.

A good example of a Private Debt Fund that is making real estate investments is Vantage Capital, the largest mezzanine fund in Africa. The firm has raised $1.6 billion across six mezzanine and renewable energy funds, and although it’s not a real estate oriented fund, it has nonetheless provided debt to several real estate projects across Africa over the years.

A newly formed private real estate debt fund is unlikely to have issues generating bankable regional deal flow. The new funds may have success approaching banks to purchase some of their performing and non-performing real estate debt. Banks are under pressure to pass stress tests and meet liquidity requirements and selling prime real estate debt could be an attractive solution. Projects that are delayed, or with a high percentage of presale defaults, might benefit from fresh private debt to remove the bank from the capital stack. Cost overruns are common in the current environment due to construction cost inflation, these projects could benefit from a bridge loan from a private debt fund.

Separately Managed and Commingled Accounts

Separately Managed Accounts (“SMAs”) permit institutional investors to set aside capital to be managed by an outside manager. The difference with this arrangement, and one involving private equity, is that with SMAs the investor maintains control and is better able to see what is actually going on. More than one investor can contribute capital through the use of commingled accounts.

SMAs are preferable to private equity because the structures are better aligned. The carry incentive is removed, and in its place, reasonable bonuses based on metrics aligned with the investors. Overinvestment will be less likely because the investors can more easily compel the manager to stop investing. Co-investments will be more likely, development risk less so, and leading syndicate rounds rare.

An example of an SMA structure operating in Latin America is Cadillac Fairview, a $40 billion dollar real estate firm that is wholly owned by the Ontario Teachers’ Pension Plan. The fund is fairly active across Latin America and has made significant investments in Colombia, Brazil and Mexico. The Canadian pension fund, PSP, is another example and in this case the manager for the Colombian real estate allocation is El Dorado Capital Advisors.